Amex Global Transfer: step by step to your first US credit card

Get a US Amex using an existing Amex from your home country, with no SSN and no US credit history. How Global Transfer works, the requirements, and the limits. For 2026.

By Chris Natterer · Published June 11, 2026

The Amex Global Transfer is the most reliable way for a non-resident to get a first real US credit card quickly. No credit score needed, no SSN, often done in a few weeks. There are requirements and one important limit, though. Both are here.

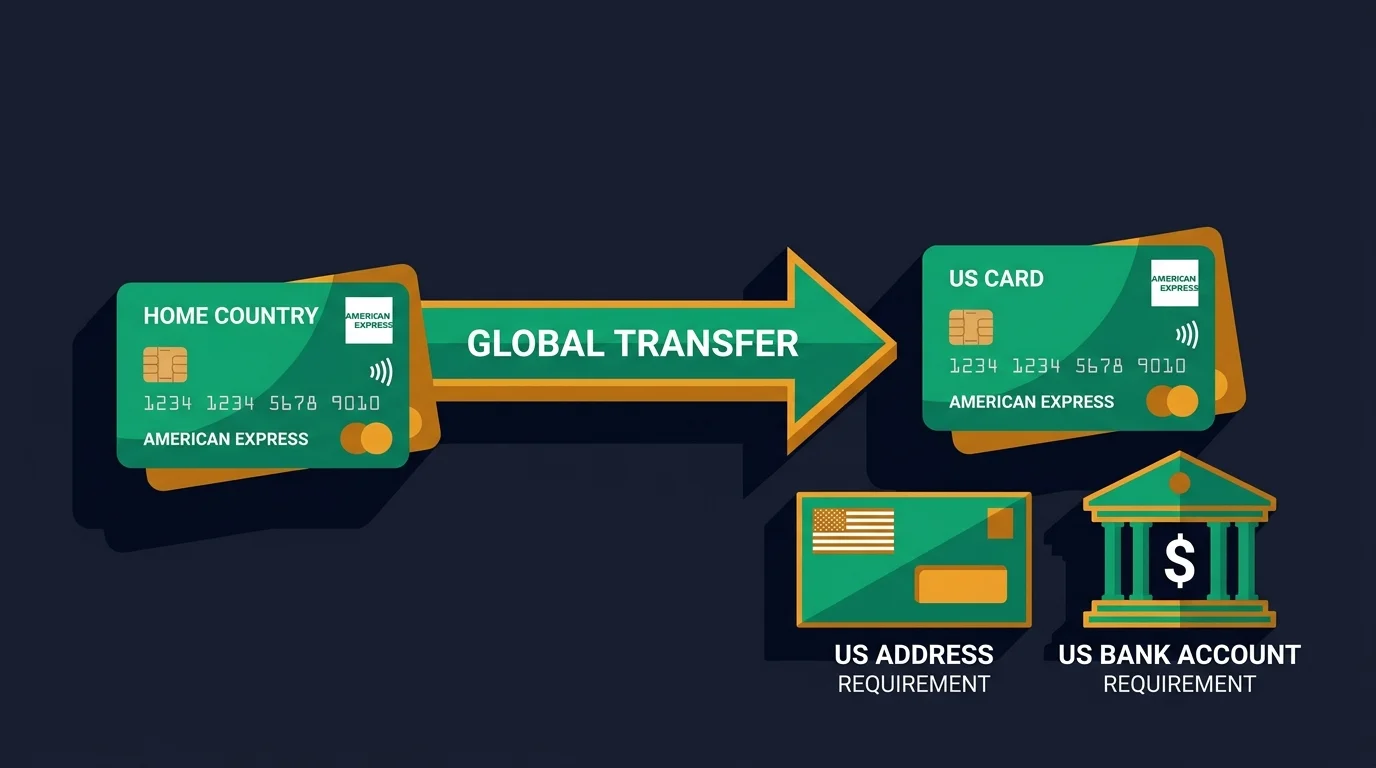

What Global Transfer is

American Express is a global company with arms in many countries. Through its Global Card Relationship, Amex lets existing customers apply for a US card when they move or build a US presence, recognizing the relationship from their home country.

The effect: Amex doesn’t treat you as a completely unknown applicant, but as an existing customer. That gets you around the biggest obstacle for newcomers, the missing US credit history. You don’t need an SSN for this route, a passport is enough for identification.

The requirements

For Global Transfer to work, four things have to be in place:

- An existing Amex in your home country, running for at least three months and in good standing. A brand-new card won’t do.

- A real US address. And one that passes as a residential or business address, not a pure mailbox or maildrop address. This is the most common stumbling block, more on that below.

- A US bank account. For the later billing and as a sign of genuine US presence.

- A valid passport for identification.

When those four things are in place, the rest is usually a formality.

Step by step

- Check your home Amex. Has it run for at least three months, paid on time? Then you’re ready to start.

- Set up the US infrastructure. The US address and US account have to exist and be consistent. For LLC owners, that comes about anyway through the business account and business address.

- Submit the Global Transfer application. This runs through the international Amex channel, not the normal US application form. You reference your existing card relationship.

- Prove your identity. Passport and, if needed, proof of address. In individual cases Amex can request additional documents.

- Receive and use the card. From here your US credit history starts running.

The limit of this route

Two things belong to the full truth.

First: this route gets you exactly one card. Global Transfer is a door-opener, not a self-service counter. A second or third US Amex you have to earn later through real US credit.

Second: the card produces only a thin history at first, a “thin file” in the jargon. You then have a US card, but not yet a workable score. To reach further attractive cards, you have to let that history grow over six to twelve months. So Global Transfer speeds up the start, but doesn’t replace building the credit score.

In individual cases American Express can request a tax transcript during the review (Form 4506). That’s no reason to worry, but it’s a hint that clean, consistent details matter.

The sore spot: the address

When an application fails, surprisingly often it isn’t the card, it’s the address. US banks recognize commercial mailbox addresses and pure maildrop services and frequently reject applications with them automatically.

You need a US address that passes as a real address and is consistent across every office: the same one at the tax authority, at the bank, and on the card application. That’s exactly why a properly set up business address through a registered agent is worth more than the cheapest maildrop service.

When Global Transfer is worth it

This route is ideal if you already have an Amex in your home country and want a first US card quickly, to start the history. If you don’t have an Amex, it isn’t the right entry point. Then the path runs through a secured card or authorized user, described in the piece on building a credit score.

The key points

- Global Transfer turns a home Amex into a US Amex, with no SSN and no US history.

- Requirements: a home Amex running for at least three months, a real US address, a US account, a passport.

- It stays at one card, and it produces only a thin history. The real score-building comes after.

- The most common reason for rejection is the address. Mailbox addresses get recognized.

How this step fits into the overall path is in the overview, US credit cards for non-residents.

This article describes the general process and is not advice. American Express’s terms change constantly. Check the current state before you apply.

Written by Chris Natterer

Founder of Globalization Guide, helping international entrepreneurs form and manage US companies since 2019.